As a healthcare provider, you might have noticed that insurance company reimbursements don’t always cover the total cost of patient consultations.

Have you ever wondered why this discrepancy occurs?

It’s all about the ‘Allowed Amount.’

Let’s delve into the intricacies of insurance procedures to shed light on the reimbursement process.

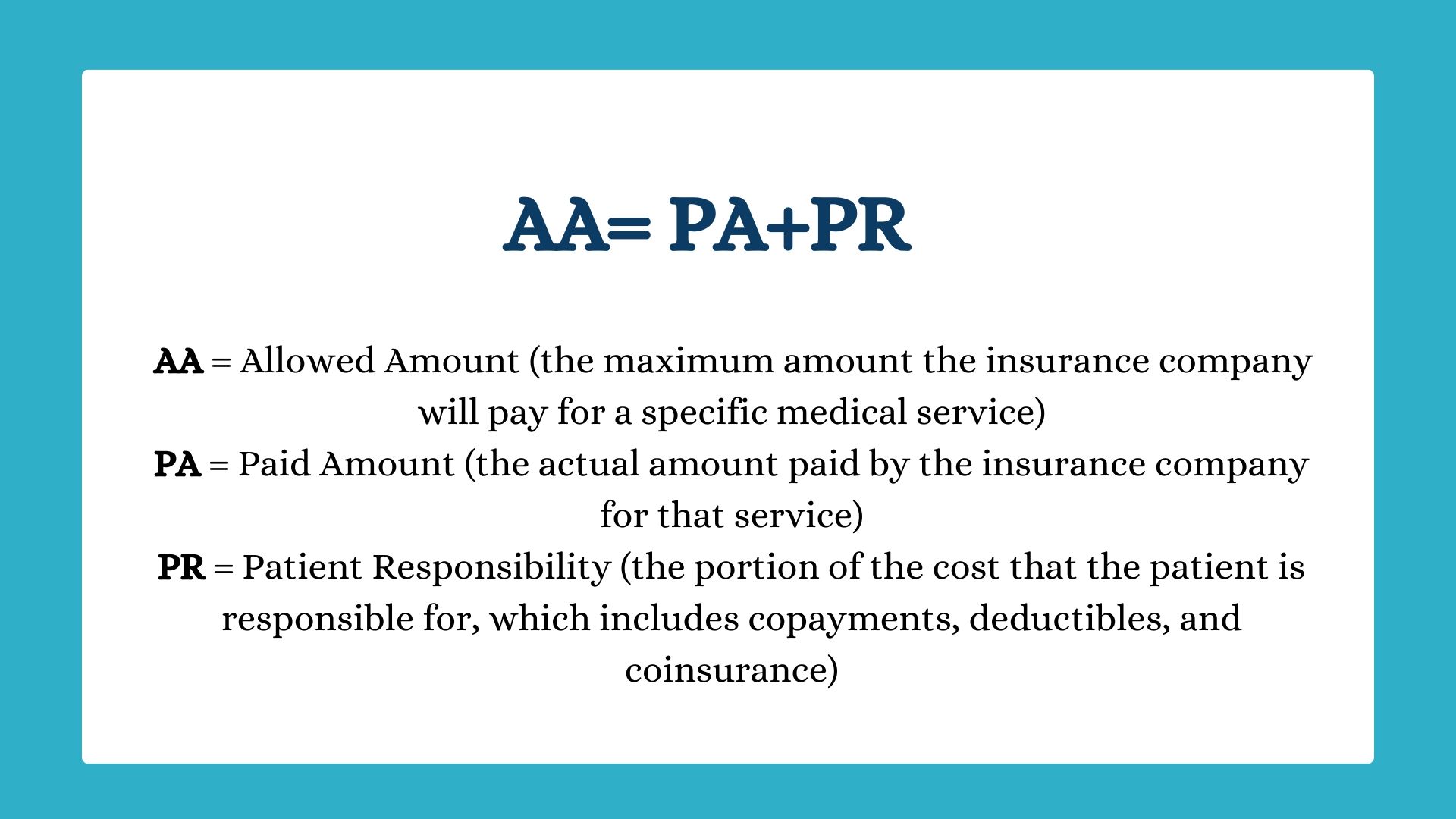

The “Allowed Amount,” also known as the “negotiated rate” or “payment allowance,” is the predetermined maximum amount that an insurance company is willing to cover for specific services, considering their fee schedule, medical policies, contractual agreements with healthcare providers or facilities, and the patient’s benefit plan with the insurance company.

The Allowed Amount differs based on whether a patient chooses an in-network or out-of-network healthcare provider. Let’s explore these distinctions.

If you’re within your patient’s healthcare plan network, i.e., providing in-network services, the allowed amount represents the predetermined, discounted price decided by their health plan for a particular service. In this case, you might present your standard fee for the service, which may be higher than the allowed amount, but you’ll be entitled to receive payment only up to the allowed amount.

Even when patients choose in-network services, they may still incur costs (copayments, coinsurance, or deductibles) depending on their health plan’s specifics. In such cases, the health insurer covers the remainder of the allowed amount based on the insurance plan’s terms.

For example, if a patient hasn’t met their deductible for the year, the insurance company may not pay anything until the deductible is met. Once the deductible is met, the insurance payer will cover some of the bill (if there’s a copay) or all of it (if there’s no copay and no coinsurance).

Picture this: If your standard charge for an office visit is $100, but the allowed amount is $80, you’ll be paid $80. If the patient is enrolled in a health plan with a $20 copay, they pay that, and the insurance covers the rest ($60). If they have a high-deductible health plan and haven’t met their deductible, they’ll be responsible for the full $80.

The advantage of being in-network lies in increased patient accessibility and the assurance of consistent, pre-established reimbursement rates. However, this also entails a contractual obligation to accept the allowed amount as the full payment.

If you’re in a health plan’s network and your charges exceed the allowed amount, they won’t be considered. You’ll be paid only the allowed amount. The Explanation of Benefits (EOB) may include a column showing the “amount not allowed,” which represents the negotiated discount between the insurance company and your practice.

If you’re outside your patient’s healthcare plan network, i.e., providing out-of-network services, the allowed amount is the price determined by the health insurance company as the appropriate fee for a specific medical service.

Since you’re not contracted with the patient’s health plan and no prearranged discount applies, you’re free to set your own price for the service. However, any reimbursement from the health plan will be determined based on the allowed amount, not the amount you initially billed.

Not all health plans cover out-of-network care except in emergencies. If your patient’s health plan does offer out-of-network coverage with cost-sharing responsibilities like coinsurance, the health plan typically determines an allowable amount based on what it deems reasonable fees rather than the provider’s charges. Your patient will be responsible for covering the remaining balance.

Health insurers assign an allowed amount for out-of-network care to manage their financial risk. Since no pre-negotiated discounts exist, this allowed amount acts as an upper-cost limit. Nevertheless, it’s important to note that this approach places the responsibility for managing excessive charges on the patient.

As a physician, you must carefully weigh the pros and cons of network participation, considering the impact on your private practice, patient care, and financial stability. Finding the right payor mix is critical to thriving in your private practice.

Schedule a Free Consultation!